Bitcoin

Biden’s Absurd 30% Tax Proposal Would Kill US Bitcoin Mining

The Biden administration recently reintroduced a proposal that would place a 30% tax on all “cryptocurrency miners” – a movement that represents an ideological witch hunt against a rapidly growing industry (see my previous comments).

The change, part of the government budget proposal for the next fiscal year introduced in March, stands in stark contrast to recent pro-crypto statements from former President Donald Trump, who this week called for the US to dominate the bitcoin mining sector. It remains to be seen whether the special tax on cryptocurrency mining will take effect (or whether Trump will enforce his aggressive crypto policies if elected), although in recent weeks many have begun to argue that President Biden may be going soft on the industry.

See too: Trump’s appeal to Bitcoin miners is a warning for crypto to remain apolitical | Opinion

It must be stated that the implementation of a 30% federal blanket tax on digital asset mining will kill the sector and wipe billions of dollars off investor value in the United States, and very likely in Canada as well, given the way the current Canadian federal administration closely follows US precedents in regulatory matters.

Taras Kulyk is founder and CEO of Sunny Side Digital.

Note: The opinions expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc. or its owners and affiliates.

In the “land of the free,” this type of heavy-handed, Stalinist central planning directive screams in the face of the democratic ideals (ironically) that should be upheld by the current White House administration. First, they came for your digital mining and you did nothing…

The fine print of Biden’s proposed tax

The egregious mining tax, implemented despite billions of dollars invested in the sector, is part of its fiscal year 2025 budget proposal, which aims to address environmental concerns and regulate the digital asset mining industry. The proposal suggests that the tax would be introduced gradually over three years, starting at 10% in the first year, increasing to 20% in the second year and reaching 30% in the third year. This tax exclusively harms digital mining, and not data centers in general.

The administration argues that the tax is necessary to combat the environmental impacts of cryptocurrency mining, including its high energy consumption and the potential for increased energy prices for communities hosting mining operations, in light of well-established research that This line of concern is the exact opposite of economic reality and the operational impact for energy companies.

The story continues

Although I am not a lawyer and these arguments should be taken with caution, it is important to note that it is likely unconstitutional for a presidential administration to tax the energy use of a specific industry. There is simply no precedent for this.

By targeting a specific industry with an energy consumption tax, the government could be seen as violating a number of clauses, including The commercial clause in Article I, Section 8, Clause 3 of the U.S. Constitution, the Equal Protection Clause found in the 14th amendment, the Due Process clause found in the Fifth Amendment of the U.S. Constitution or under the unintended consequences status.

Furthermore, there are ethical implications at play that go beyond any potential unconstitutional excess. This type of deception has become all too common and is something the US founders were aware of and tried to prevent through the Constitution itself.

How to kill an emerging industry 101

The tax proposed by the Biden administration would impose a significant financial burden on digital mining companies, most likely making their operations economically unviable. Given that these companies already face intense competition and tight margins, this tax would only worsen financial difficulties and lead to material losses for investors.

As a result, many mining companies would likely be forced to close or relocate to other countries with more favorable tax policies, leading to job losses and reduced economic activity in the United States.

Furthermore, the proposed tax would disproportionately affect smaller digital mining operations, which may not have the resources to absorb the additional costs or to relocate to other jurisdictions. This would create an uneven playing field, favoring larger, more established mining companies and stifling competition and innovation in the sector, as well as increasing centralization for larger operators.

If this administration’s goal is to harm small businesses, stifle innovation and develop a reputation for reducing economic activity in the US, then they are on the right track.

Environmental concerns and the ineffectiveness of the tax

The Biden administration claims the proposed tax is necessary to address the environmental impact of bitcoin mining, as it consumes significant amounts of electricity. However, this argument ignores the fact that many mining operations already use renewable energy sources and are actively working to reduce their carbon footprint.

Furthermore, the proposal does not take into account the use of methods such as methane burning, which reduces CO2 equivalent emissions by around 63% when compared to traditional methods of burning methane and mining in landfills, which in one year have the same effect of plant five million trees and let them grow for 10 years. It has been proven that Bitcoin mining strengthen networks and even reduce energy costs for local communities.

In fact, imposing a tax on energy consumption could discourage these efforts and encourage miners to use less environmentally friendly energy sources abroad. What will happen is a mass exodus of miners out of the US, which has the largest renewable energy composition, and transfer them abroad, where fossil fuels are more predominantly used.

The fact is that, about 90% of carbon emissions come from outside the United States. Since addressing “environmental concerns” is a global problem, they would only be contributing to the problem through their own logic.

So what should the government do? Anything. Let the free market reign. Bitcoin miners are the energy beetles. They go where energy is cheapest, and given the initial operating expenses of fossil fuel miners and the low operating expenses of renewables, it’s easy to see why most mining comes from renewable sources.

Global competition

The bitcoin mining industry is highly competitive, with countries like China, Russia and Canada vying for dominance. The proposed tax would harm the United States’ position in this global race, as it would make the country a less attractive destination for mining operations. This could result in a significant loss of investment, talent and technological advances, ultimately weakening the United States’ role in the digital economy.

A lesson learned later China banned bitcoin mining in 2021 it was the resilience and adaptability of the bitcoin mining industry. Despite the ban, bitcoin mining operations have found new homes in countries with more favorable regulatory environments and access to renewable energy sources. This demonstrated that the Bitcoin network is not geographically confined and can adjust to regulatory changes.

Furthermore, the shift to more sustainable energy sources has highlighted the potential for bitcoin mining to positively contribute to the global energy transition.

Furthermore, the tax could also have broader implications for the cryptocurrency industry as a whole. By targeting bitcoin mining, the Biden administration may inadvertently discourage innovation and investment in the industry, which could have far-reaching consequences for the country’s technological development and competitiveness.

You can’t ban mining, you can only ban yourself

In short, the Biden administration’s proposed tax on bitcoin mining would have serious negative consequences for the industry and the broader digital economy in the United States, and therefore for its own initiatives.

See too: Bitcoin Miners Show Resistance Against Unwarranted EIA Survey

It would impose a significant financial burden on mining companies, discourage sustainable mining practices and harm the country’s competitiveness in the global market. This type of measure is more in line with oppressive countries like China or the USSR, and it is incredibly disheartening to see this in the United States.

Just as the industry came together to defeat the unconstitutional EIA research, we must place the same attention here. You cannot ban Bitcoin mining, you can only ban yourself.

Bitcoin Currency

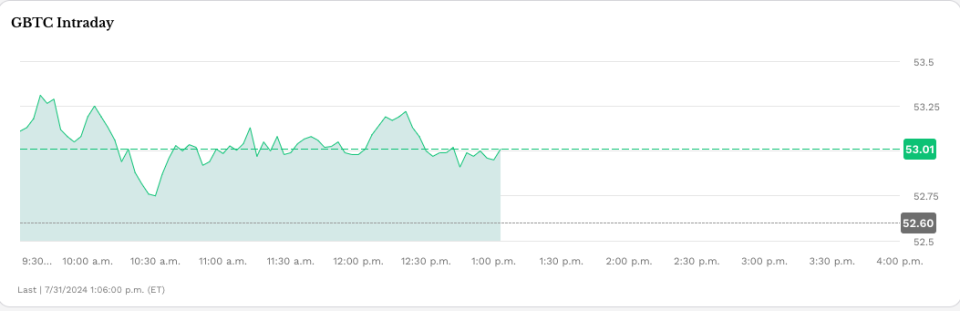

Grayscale Investments The Bitcoin Mini Trust began trading on Wednesday with a 0.15% expense ratio, offering a lower-cost option for bitcoin exposure in the market.

The Mini Trust, which has the symbol BTC and trades on NYSE Arca, is structured as a spin-off of the Grayscale Bitcoin Trust (GBTC). New shares will be distributed to existing GBTC shareholders with the fund contributing a portion of its bitcoin holdings to the new product. According to a company press releaseBTC’s S-1 registration statement became effective last week.

“The Grayscale team has believed in the transformative potential of Bitcoin since the initial launch of GBTC in 2013, and we are excited to launch the Grayscale Bitcoin Mini Trust to help further lower the barrier to entry for Bitcoin in an SEC-regulated investment vehicle,” said David LaValle, Senior Managing Director and Head of ETFs at Grayscale.

The Bitcoin Mini Trust’s debut comes amid growing interest in ETFs based on the current price of the two largest cryptocurrencies by market cap, bitcoin and ether. Spot bitcoin ETFs have generated nearly $18 billion in inflows since the first ones began trading on Jan. 11, though GBTC has lost nearly $19 billion in assets.

This fund differs from other funds because it is a conversion of an existing fund and has a 1.5% fee, the highest among spot bitcoin products that have received SEC approval this year.

Mini Bitcoin Trust Low Fee

On a Post X On Wednesday, Bloomberg senior ETF analyst Eric Balchunas noted the Bitcoin Mini Trust’s “lowest fee in the category…”

“[Important] to recognize how incredibly cheap 15bps is — about 10x cheaper than spot ETFs in other countries and other vehicles,” Balchunas wrote, adding that this pricing strategy reflects the competitive nature of the U.S. ETF market, which he referred to as the “ETF Terrordome.”

“This is what Terrordome does to fund [cost]. It reaches 1.5% [and] end in 0.15%, how to go from [a] country club to the jungle. But that’s why all the flows are here, investor paradise,” he noted.

Read more: Spot Bitcoin ETF Inflows Hit Daily High of Over $1 Billion

Bitcoin was recently trading at around $66,350, virtually flat since U.S. markets opened on Wednesday.

Grayscale also offers two spot Ethereum ETFs, the Grayscale Ethereum Trust (ETHE) and the Grayscale Ethereum (ETH) Mini Trustwhose performance is based on ETHE. ETHE outflows exceeded $1.8 billion in its first six days of trading, while ETH added more than $181 million in the same period, according to Farside. The remaining seven ETFs generated about $1.2 billion in inflows.

The story continues

Read more: Spot Ethereum ETFs Approved to Start Trading

Permanent link | © Copyright 2024 etf.com. All rights reserved

Cryptocurrencies fell sharply on Wednesday as rising geopolitical risks captivated investors’ attention following the conclusion of the Federal Reserve’s July meeting.

Bitcoin (BTC) fell to $64,500 from around $66,500, where it traded following Federal Reserve Chairman Jerome Powell’s press conference and is down more than 2% in the past 24 hours. Major altcoins including ether (ETH)sunbathing (SUN)Avalanche AVAX (AVAX) and Cardano (ADA) also fell, while Ripple’s XRP saved some of its early gains today. The broad cryptocurrency market benchmark CoinDesk 20 Index was 0.8% lower than 24 hours ago.

The liquidation happened when the New York Times reported that Iran’s leaders have ordered retaliation against Israel over the killing of Hamas leader Ismail Haniyeh in Tehran, raising the risk of a wider conflict in the region.

Earlier today, the Fed left benchmark interest rates unchanged and gave little indication that a widely expected rate cut in September is a given. The Fed’s Powell said that while no decision has been made on a September cut, the “broad sense is that we are getting closer” to cutting rates.

While digital assets suffered losses, most traditional asset classes rose higher during the day. U.S. 10-year bond yields fell 10 basis points, while gold rose 1.5% to $2,450, slightly below its record highs, and WTI crude oil prices rose 5%. Stocks also rallied during the day, with the tech-heavy Nasdaq 100 index rebounding 3% and the S&P 500 closing the session 2.2% higher, led by 12% gains in chipmaker giant Nvidia (NVDA).

The different performances across asset classes could be due to traders’ positioning ahead of the Fed meeting, Zach Pandl, head of research at Grayscale, said in an emailed note.

“Equities may have been slightly underutilized after the recent dip, while bitcoin is coming off a strong period with solid inflows, while gold has recovered after a period of weakness,” he said.

“Overall, the combination of Fed rate cuts, bipartisan focus on cryptocurrency policy issues, and the prospect of a second Trump administration that could advocate for a weaker U.S. dollar should be viewed as very positive for bitcoin,” he concluded.

UPDATE (July 31, 2024, 21:30 UTC): Adds grayscale comments.

Former US President Donald Trump spoke at the Libertarian National Convention in May and lent his a strong support to crypto: “I will also stop Joe Biden’s crusade to crush crypto. … I will ensure that the future of crypto and the future of bitcoin is made in the US, not taken overseas. I will support the right to self-custody. To the 50 million crypto holders in the country, I say this: With your vote, I will keep Elizabeth Warren and her henchmen out of your bitcoin.”

Former US President Donald Trump spoke at the Libertarian National Convention in May and lent his a strong support to crypto: “I will also stop Joe Biden’s crusade to crush crypto. … I will ensure that the future of crypto and the future of bitcoin is made in the US, not taken overseas. I will support the right to self-custody. To the 50 million crypto holders in the country, I say this: With your vote, I will keep Elizabeth Warren and her henchmen out of your bitcoin.”

Trump continued to court the cryptocurrency industry in the months that followed; he he appeared at the Bitcoin 2024 Conference in Nashville this week, along with independent presidential candidate Robert F. Kennedy Jr.’s parting words to Trump — “Have fun with your bitcoin, your cryptocurrency and whatever else you’re playing with” — were less than enthusiastic, but the industry itself remains packed with ardent Trump supporters.

This turnaround came as a surprise, given Trump’s previous strong opposition to cryptocurrency. When Facebook was floating its Libra cryptocurrency in 2019, Trump tweeted: “I am not a fan of Bitcoin and other cryptocurrencies, which are not money, and whose value is highly volatile and based on thin air.” Former national security adviser John Bolton’s White House memoir, The Room Where It Happened, quotes Trump as telling Treasury Secretary Steven Mnuchin: “Don’t be a trade negotiator. Go after Bitcoin.” [for fraud].” In 2021, Trump counted Fox Business that bitcoin “just looks like a scam. … I want the dollar to be the world’s currency.”

Why the change? There doesn’t seem to be any crypto votes. Trump’s “50 million” number comes from a poorly sampled push survey by cryptocurrency exchange Coinbase which claimed 52 million cryptocurrency users in the United States starting in February 2023. But one survey A survey conducted last October by the US Federal Reserve showed that only 7% of adults (about 18.3 million people) admitted to owning or using cryptocurrencies — down from 10% in 2022 and 12% in 2021. Many of these people are likely wallet owners who were left holding the bag after crypto plunged in 2022 — and are not necessarily new fans.

What Trump wants from the cryptocurrency industry is money. The cryptocurrency industry has already raised more than US$ 180 million to run in the 2024 US elections through his super PACs Fairshake, Defend American Jobs and Protect Progress.

Fairshake spent $10 million on taking Rep. Katie Porter in the primary battle for Dianne Feinstein’s California Senate seat by funding Porter’s pro-crypto rival Adam Schiff. This put $2 million to knock out Rep. Jamaal Bowman in the Democratic primary for New York’s 16th District in favor of pro-crypto George Latimer. In the Utah Senate Republican primary, Rep. John Curtis defeated Trent Staggs with the help of $4.7 million from Defend American Jobs. In Alabama’s House District 2, the majority of campaign expenses came from the cryptocurrency industry.

Fairshake is substantially financed by Coinbase, cryptocurrency issuer Ripple Labs, and Silicon Valley venture capital firm Andreessen Horowitz, or a16z. Silicon Valley was awash in cryptocurrencies during the 2021 bubble, and a16z in particular continues to promote blockchain startups to this day — and still holds a huge amount of bubble crypto tokens that he wishes he could cash in on.

Many in Silicon Valley would like an authoritarian who they think will let them run wild with money — while bailing them out in tough times. Indeed, Trump promised Bitcoin 2024 participants that he hold all bitcoins that the United States acquires. (Never mind that it is usually acquired as the proceeds of crime.) Silicon Valley explicitly sees regulation of any kind as its greatest enemy. Three a16z manifestos — “Politics and the Future” It is “The Techno-Optimist Manifesto” and 2024 “The Small Tech Agenda—describe co-founders Marc Andreessen and Ben Horowitz’s demands for a technology-powered capitalism unhindered by regulation or social considerations. They name “experts,” “bureaucracy,” and “social responsibility” as their “enemies.” Their 2024 statement alleges that banks are unfairly cutting off startups from the banking system; these would be crypto companies funded by a16z.

Trump’s vice presidential pick, Senator J.D. Vance, is a former Silicon Valley venture capitalist. He was once employed by Peter Thiel, who bankrolled Vance’s successful 2022 Senate run; Vance has been described as a “Thiel creation”. He has increased support for the Trump ticket among his venture capital associates. Vance is a bitcoin holder and a frequent advocate of encryption. He recently released a draft bill to review how the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) control crypto assets. In 2023, he circulated a bill to prevent banks from cutting out cryptocurrency exchanges.

Minimal regulation has been tried before. It led to the wild exuberance of the 1920s, which ended with the Black Tuesday crash of 1929 and the Great Depression of the 1930s. Regulators like the SEC were put in place during this era to protect investors and transform the securities market from a jungle into a well-tended garden, leading to many prosperous and stable decades that followed.

Crypto provides the opposite of a stable and functional system; it is a practical example of how a lack of regulation allows opportunists and scammers to cause large-scale disasters. The 2022 Crypto Crash repeated the 2008 financial crisis in miniature. FTX’s Sam Bankman-Fried was feted as a financial prodigy who would perform economic miracles if you just gave him carte blanche; he ended up stealing billions of dollars of customers’ money, destroying the lives of ordinary people, and is now in a prison cell.

U.S. regulators have long been concerned about the prospect of cryptocurrency contagion to the broader economy. Criminal money laundering is rampant in cryptocurrency; even the Trump administration has made rules in December 2020 to reduce the risk of money laundering from crypto. Meanwhile, the crypto industry has persistently tried to infiltrate systemically risky corners of the economy, such as pension funds.

Four U.S. banks collapsed during the 2023 banking crisis, the first since 2020. Two of them, Silvergate Bank and Signature Bank, were deeply embedded in the crypto world — Silvergate in particular appears to have collapsed directly from its heavy reliance on FTX and failed a few months after that. Silicon Valley Bank was not involved in crypto but collapsed due to a run on the bench due to panic among venture capital deposit holders, particularly Thiel’s Founders Fund.

Project 2025the Heritage Foundation mammoth conservative wish list The plan, which Trump and Vance have both endorsed and tried to distance themselves from at various times, emphasizes the importance of party loyalists, noting especially financial regulation. The plan recommends replacing as much of the federal bureaucracy as possible with loyalists and “trusted” career officials rather than nonpartisan “experts.” Vance defended in 2021 that Trump should “fire every mid-level bureaucrat, every civil servant in the administrative state” and “replace them with our people.” Loyalty will likely trump competence.

Crypto is barely mentioned directly in Project 2025 — suggesting it has little active support among the broader conservative coalition. But near the end of the manifesto is a plan to dismantle most U.S. financial regulations and investor protections put in place since the 1930s, suggesting the exemption the crypto industry seeks from current SEC and CFTC regulations.

Bitcoin, the first cryptocurrency, started as an ideological project to promote a strange variant of Murray Rothbard’s anarcho-capitalism and the Austrian gold-backed economy—the kind we abandoned to escape the Great Depression. Crypto quickly co-opted the “end of the Fed” and “establishment elites” conspiracy theories of the John Birch Society and Eustace Mullins. It’s a way for billionaire capitalists like Thiel, Andreessen and Elon Musk to claim they’re not part of the so-called elite.

If a second Trump administration were to limp along with financial regulators and allow cryptocurrencies to have free rein, it could help foster the collapse of the U.S. economy that bitcoin claimed to prevent. But Trump is more likely to be happy to take the crypto money and run.

Donald Trump’s recent promise to create a “strategic national stockpile of Bitcoin” may not turn out to be as big a commitment as the hype surrounding the announcement makes it seem.

“Trump’s proposal is extremely modest,” said George Selgin, director emeritus of the Center for Monetary and Financial Alternatives at the Cato Institutea Washington-based public policy group. “It doesn’t have much economic implication.”

It started !! → Trump has just sent Crypto Nuclear! Buy these 15 coins now (urgent AF)

Just in: The United States approves the historical legislation of cryptocurrencies .. what is the next?

0.1 bitcoin = luxury life

Altcoin’s season starts now! 3 experts discuss the price of Bitcoin price in 2025

Having only .1 Bitcoin will change your life | Eric Trump

Ethereum Posts First Consecutive Monthly Losses Since August 2023 on New ETFs

Cryptocurrency Regulation in Slovenia 2024

New bill pushes Department of Veterans Affairs to examine how blockchain can improve its work

Think You Own Your Crypto? New UK Law Would Ensure It – DL News

Upbit, Coinone, Bithumb Face New Fees Under South Korea’s Cryptocurrency Law

It started !! → Trump has just sent Crypto Nuclear! Buy these 15 coins now (urgent AF)

Just in: The United States approves the historical legislation of cryptocurrencies .. what is the next?

0.1 bitcoin = luxury life

Altcoin’s season starts now! 3 experts discuss the price of Bitcoin price in 2025

Having only .1 Bitcoin will change your life | Eric Trump

-

Ethereum12 months ago

Ethereum12 months agoEthereum Posts First Consecutive Monthly Losses Since August 2023 on New ETFs

-

Regulation12 months ago

Regulation12 months agoCryptocurrency Regulation in Slovenia 2024

-

News12 months ago

News12 months agoNew bill pushes Department of Veterans Affairs to examine how blockchain can improve its work

-

Regulation12 months ago

Regulation12 months agoThink You Own Your Crypto? New UK Law Would Ensure It – DL News

-

Regulation12 months ago

Regulation12 months agoUpbit, Coinone, Bithumb Face New Fees Under South Korea’s Cryptocurrency Law

-

Regulation12 months ago

Regulation12 months agoA Blank Slate for Cryptocurrencies: Kamala Harris’ Regulatory Opportunity

-

Regulation12 months ago

Regulation12 months agoBahamas Passes Cryptocurrency Bill Designed to Prevent FTX, Terra Disasters

-

Regulation12 months ago

Regulation12 months agoIndia to Follow G20 Policy for Cryptocurrency Regulation: MoS Finance

-

News1 year ago

News1 year ago“Captain Tsubasa – RIVALS” launches on Oasys Blockchain

-

Ethereum1 year ago

Ethereum1 year agoComment deux frères auraient dérobé 25 millions de dollars lors d’un braquage d’Ethereum de 12 secondes • The Register

-

News12 months ago

News12 months agoEU supports 15 startups to fight online disinformation with blockchain

-

News1 year ago

News1 year agoSolana ranks the fastest blockchain in the world, surpassing Ethereum, Polygon ⋆ ZyCrypto