News

What Happened To Those Bull Market Corporate Blockchain Projects?

JPMorgan Chase CEO Jamie Dimon has repeatedly criticized bitcoin and other cryptocurrencies. But … [+] his firm has remained a leader in developing blockchain-based products and services.

Getty Images

Over the course of the last crypto bull market, many large financial services firms announced various projects and products based on blockchain technology. The 2020-2022 crypto bull market ended with the high-profile bankruptcy of Three Arrows Capital, FTX and others. The collapse of the bull market took blockchain technology out of the spotlight. Two years later, crypto prices are once again surging, and it’s a good opportunity to look back at all of those corporate blockchain projects from the last bull market to see what happened.

Since so much of the coverage of crypto and blockchain shows a strong bias for or against the technology, this piece will strive to be unbiased when examining the top blockchain use cases for established financial services firms. It will highlight both positive (continued traction) and negative (lack of traction) examples.

What is blockchain technology?

Before diving in, here’s a brief review of the blockchain concept and how it’s distinct from cryptocurrencies like bitcoin

BTC

and ethereum

ETH

. At its most basic level, a blockchain is a decentralized database shared between multiple parties. It is either publicly viewable or is only viewable to certain parties. Because blockchains are decentralized—and not controlled by a single party like a traditional database structure—they operate using “smart contracts.” Smart contracts automatically execute, control and document events and actions according to preset parameters.

Blockchain technology is the innovation that enabled the rise of independent cryptocurrencies like Bitcoin and Ethereum. But the technology can be used for other purposes as well, ranging from insurance to bond trading. For an example of this distinction, over the years JPMorgan Chase

JPM

CEO Jamie Dimon has derided bitcoin and other independent cryptocurrencies as a “fraud,” a “waste of time,” and a “pet rock.” Yet despite these extremely negative statements about cryptocurrencies, JPMorgan Chase has been a leader in building blockchain-based solutions for banking and trading.

According to Mike Pavel, head of strategy at ZK Ladder, a SaaS platform that lets companies connect physical things with blockchain records using NFC chips, “blockchains and cryptocurrencies are often conflated in the collective mind of the public. For example, at ZK Ladder, we have been hyper-focused on articulating both our product and our messaging to ensure a clear understanding of the differences. Blockchain technology companies like ZK Ladder are not selling speculative coins.”

There are two key caveats to keep in mind before proceeding. First, I am discussing what the largest global financial firms are doing with blockchain technology. There is an entirely separate decentralized finance ecosystem (known as “DeFi”) that is building decentralized financial products without any traditional intermediaries and large financial firms. For example, Centrifuge

CFG

claims to have financed $544 million working with DeFi protocols. A detailed examination of the state of DeFi is a topic for another day.

Second, it is worth noting that I am relying on publicly available information and announcements, with the general assumption that if a firm has not provided any update on a blockchain initiative years after the initial announcement, the project has either been canceled or put on hold. In some cases, that may not be a correct assumption.

Large banks show interest in blockchain

Large banks have continued to invest in and develop blockchain-based solutions for banking and payments throughout the crypto bear market. Depending on definitions, there are five high-profile blockchain consortiums/joint initiatives in the banking and payments space.

First, the bank-led Regulated Liability Network initiative started live tests in both the U.S. and the U.K. in 2023. Second, the Universal Digital Payments Network is backed by 25 different organizations and has 12 proof of concepts running. Third, there is the R3 initiative, which received $107 million of funding from a group of banks in 2017 (note that as of 2024, however, the R3 initiative seems to be more focused on brokerage/trading use cases). Fourth, Fnality International is backed by 20 major institutions and notably launched a Sterling-based payment system in December 2023. Finally, there is Ripple, who has worked with several large banks. While the firm has been embroiled in a high-profile legal battle with the Securities and Exchange Commission for the last few years, Ripple continues to build crossborder payment services.

The SWIFT messaging system is arguably the best-known example of the technology behind the current … [+] global interbank payments system.

Bloomberg

According to Kevin Goldstein, managing partner at Kee Global Advisors, “Even if the benefits of the technology incentivize adoption, building a consortium is a slow and steady process. Wall Street banks can sometimes struggle with collaboration, so these consortiums will have to work out thorny issues between parties. And as these projects scale up, they will also likely need to carefully manage regulatory issues and avoid creating the perception that a consortium is reducing competition.”

When it comes to individual banks, JPMorgan Chase stands out for its pursuit of blockchain-based products and services. JPMorgan Chase has set up a dedicated blockchain group (dubbed “Onyx”) and has developed the JPMCoin stablecoin that has processed over $1 billion in transactions. JPMorgan Chase has also created a blockchain (dubbed “Liink”) that can facilitate cross-border payments.

In addition, JPMorgan Chase is heavily involved in the joint venture Partior. DBS

DBS

Bank, Standard Chartered and the Government of Singapore are also involved in the Partior joint venture. In May 2023, JPMorgan Chase received approval to use Partior from the United States’ Office of the Comptroller of the Currency. The firm took their JPMCoin live on Partior in December 2023.

Outside of JPMorgan Chase, however, it seems that many banks have stopped pursuing proprietary blockchain banking/payments projects. Over the years, various large established financial institutions had announced blockchain-related pilots and products. Examples range from the BNP Paribas project launched in 2016 to more recent examples from BBVA (announced in 2020) and HSBC

HBA

and Wells Fargo

WFC

(announced in 2021). I was unable to find recent updates on the various blockchain projects led by only one or two banks. Outside of JPMorgan Chase, it seems that most banks may be opting to participate in consortiums and joint projects.

The shift to consortiums and joint projects likely reflects the fact that most banking and payment activities require numerous counterparties. JPMorgan Chase is the world’s largest bank by market capitalization and by a wide margin. While JPMorgan Chase has the resources and heft to try to build their own blockchain network, most banks have likely realized that they’ll be unable to build their own blockchain and attract a sufficient number of other banks to create the needed “network effects.”

The world’s largest bank by market capitalization has been developing blockchain-based products and … [+] services.

Getty Images

According to Corbin Norman, startup advisor and former marketing leader at a neobank, “Blockchain innovation thrives on collaboration. Consortiums and joint ventures are the go-to strategy, enabling relatively smaller players to unlock the power of blockchain in banking and payments. While the long-term winners have yet to be decided, widespread adoption will eventually happen.”

Blockchain projects at brokerages

Like banking and payments, the brokerage and trading industry has continued to see strong adoption and interest in blockchain technology despite the crypto bear market. Brokerage firms look to blockchain technology and tokenized versions of investment products to improve efficiency, reduce costs, and/or to remove intermediaries. In the last twelve months alone, there have been many examples of large financial services firms announcing the launch or expansion of brokerage-related blockchain projects. Examples include BNP Paribas, Citi, Franklin Templeton, HSBC, J.P. Morgan, Societe Generale, WisdomTree, and UBS. In a sign of the disruptive potential blockchain poses to brokerage and trading, in December 2023 DTCC (the largest clearing and settlement firm in the world) bought blockchain company Securrency.

The CEO of the world’s largest asset manager, BlackRock

BLK

, has notably made multiple public statements about the impact blockchain technology will have on the asset management industry. BlackRock launched a tokenized money market fund in March 2024, raising $160M in the first week.

Larry Fink, the CEO of the world’s largest asset manager, has made multiple public statements about … [+] the impact blockchain technology will have on the asset management industry.

getty

Although there are some examples of consortiums and joint blockchain projects/initiatives in the brokerage space (example), compared to the banking and payments use cases outlined above, more firms are pursuing their own initiatives. This difference stems from the fact that blockchain-based brokerage and trading services can be offered to clients with fewer counterparties than banking and payments services require.

Insurance players seem to step away

Now we’ll switch gears and talk about two financial services use cases where the outlook for blockchain technology is at best unclear or at worst failing to live up to the hype. In the insurance space, the B3i insurance blockchain initiative (backed by several large insurance firms) ceased operations in July 2022. The project was shut down only a few months after starting active pilots.

A survey from BCG in November 2023 found that 60% of insurance companies are already investing in blockchain technology, but there isn’t much public evidence of the investment noted in the BCG survey. I haven’t been able to find updates on individual blockchain initiatives launched in the last crypto bull market, such as the USAA/State Farm blockchain project (launched in 2021) or the Allianz blockchain project for auto insurance (launched in 2021). The Riskstream alliance—founded in 2019 and backed by several large insurance firms—is still active, but compared to the banking and brokerage use cases, there seems to be much less traction in the insurance industry.

The insurance claims process can sometimes be clunky and slow. The means that use case for … [+] blockchain and smart contracts is less compelling.

Getty Images

The nature of insurance claims means that the value of a shared blockchain and automated smart contracts is less compelling compared to the more straightforward and often near-instantaneous task of processing a payment or a trade. Insurance claims sometimes involve lengthy in-person investigations and disputes that end up in court.

Moreover, the insurance industry is known to be relatively slow to adapt to new technology. The industry does not appear to be willing to undertake a complex transformation from old IT systems to a shared blockchain-based approach.

Not much traction across real estate

During the 2020-2022 crypto bull market, much ink was spilled on the potential for blockchain to improve elements of the real estate industry, such as the mortgage ecosystem, real estate transactions, the land registry process, etc. Like the insurance industry, however, it is difficult to find up-to-date information on the various blockchain projects undertaken by the largest real estate firms. For example, I could not find any recent updates on Coldwell Banker’s project to tokenize real estate (announced in January 2022) or RE/MAX’s

RMAX

partnership with XYO network to build a land registry in Mexico (first announced in 2018).

Over the years, several real estate blockchain startups have touted partnerships or case studies with the largest players in the industry (RE/MAX example), but once again it is hard to find up-to-date information here and/or evidence that the largest real estate firms have started working with these tech companies on a meaningful scale.

When discussing real estate blockchain projects, it is worth noting that national and subnational governments have made various announcements over the years about facilitating real estate transactions on a blockchain. Examples of these government initiatives include the Swedish government (first announced in 2016), the UAE

UAE

government (first announced in 2019), and the U.K. government (first announced in 2019). It is difficult to find up-to-date information on the current status of various government-level real estate blockchain initiatives, but the UAE initiative appears to be active as of at least 2023.

Earlier claims about the potential for blockchain to disrupt real estate do not seem to have panned … [+] out.

Getty Images

The key players in the established real estate industry—real estate agents, lenders, local governments and data vendors—do not seem to have the right incentives necessary to incentivize blockchain adoption.

Financial services is not a monolith

This piece has hopefully given you a better perspective on which use cases still have meaningful traction among the largest global financial firms in 2024. The outlook for blockchain in the insurance and the real estate sector is uncertain. Even in the brokerage and banking/payments space—where the established financial players continue to show strong interest in blockchain technology—the transition will likely take two to five years.

Financial infrastructure is a very complex and highly regulated space. Key components of financial markets and global payments will not be moving to shared blockchains quickly. But there is real interest and traction when it comes to blockchain in certain areas of financial services—the technology is not just hype and froth.

According to Diederick Van Thiel, cofounder and CEO of AdviceRobo, a fintech company that helps banks improve credit management by providing unique data points on customers and AI-based financial wellness solutions, “through my work as both CEO of AdviceRobo and non-executive director in neo-banking and private equity, I have been exposed to many large financial services firm’s complex infrastructure and often siloed databases. It will take time, but the right use cases, like the movement of money and assets within and across countries, benefit from a shared blockchain approach.”

Disclosure: The views and opinions expressed here are solely those of the author and do not represent the views and opinions of the crypto.news editorial team.

Access to clean water is a basic human need, yet billions of people around the world still struggle to get it. According to the World Health Organization, over 2 billion people live in countries suffering from severe water stress, and this number is expected to continue to grow due to climate change and population growth.

Traditional water management systems have struggled to address these challenges, often hampered by inefficiencies, lack of transparency, and misallocation of resources. Blockchain technology offers a promising solution to these challenges, providing equitable access and sustainable use of this crucial resource.

The current state of water management

Water management today faces several pressing issues. Inefficiencies in water supply, distribution, and use, coupled with a lack of real-time monitoring, often result in resource waste and misallocation. Many water sources fail to realize their full potential due to infrastructure and financing shortfalls. For example, the Environmental Protection Agency (EPA) report indicated that the United States would need to invest $625 billion over the next 20 years to repair, maintain and improve the country’s drinking water infrastructure due to aging pipes and other infrastructure problems. Additionally, in the United States alone, household leaks can to waste nearly 900 billion gallons of water per year nationwide. This is equivalent to the annual domestic water consumption of nearly 11 million homes.

Furthermore, corruption and mismanagement of water resources can cause unequal distribution, with disadvantaged communities often bearing the brunt of water scarcity. For example, South Africa is struggling with myriad challenges to its water security: drought, inadequate water conservation measures, outdated infrastructure, and unequal access to water resources. The country faces significant water scarcity, with demand expected to outstrip supply by 2030, creating a projected gap of 17%.

Furthermore, the global water industry is highly monopolized, with a few key players controlling a significant share of the market. These companies exert substantial influence over the water supply chain, often prioritizing profit over equitable distribution and environmental responsibility. This concentration of power can lead to inflated prices and limited access for vulnerable populations. The global bottled water market alone is projected to reach $509.18 billion by 2030, with these large companies capturing a significant share of revenue. This monopolization exacerbates existing inequalities in water access and highlights the need for more decentralized and community-driven water management solutions.

Source: Grand View Search

The potential of blockchain in water management

Blockchain technology can address these issues by providing a transparent, secure, and decentralized platform for water resource management. This approach offers several advantages:

- Transparency and accountability. Blockchain’s immutable ledger ensures that all transactions and data entries are transparent and cannot be changed once recorded. This transparency can reduce corruption and ensure that water resources are allocated fairly and efficiently. For example, blockchain can be used to track water usage from source to end user, providing a clear record of how water is distributed and used. This level of transparency can help hold authorities accountable and manage water resources sustainably.

- Efficient resource management. Blockchain can facilitate the creation of smart contracts, which are self-executing contracts with the terms of the agreement written directly into the code. These contracts can automate water distribution based on real-time data, directing water to where it is needed most. For example, smart contracts could be used to manage urban water supply systems, automatically adjusting water distribution based on real-time consumption patterns and demand. This can help optimize water use, reduce waste, and ensure that households and businesses receive the right amount of water at the right time.

In Dubai, the Dubai Electricity and Water Authority (DEWA) has implemented a blockchain-based smart water network initiative as part of its broader smart city strategy. This project integrates blockchain technology with IoT sensors to monitor water usage in real time, manage distribution, and detect leaks. The decentralized ledger ensures data integrity and transparency, enabling more efficient water management and reduced waste. DEWA’s initiative aims to improve sustainability and resource management in the rapidly growing city, highlighting the potential of blockchain to support urban water management and conservation efforts.

Community participation and ownership

Through blockchain, individuals can directly control and monetize their access to water resources, eliminating the need for third-party intermediaries. This direct control model allows local communities to make collective and transparent decisions about their water use. By managing their water directly from the source, communities can tailor water management practices to their specific needs, promoting equitable distribution and encouraging a sense of accountability and stewardship.

Additionally, future models could allow people to monetize their access to water through web3 technologies. For example, a community-to-business (C2B) model could allow people to sell water directly to companies. In this model, people do not have to own the water directly, but can profit by staking their tokens during event sales pools. This approach not only supports sustainable water management, but also creates economic opportunities for community members. Additionally, a “Burn to Secure” protocol can be used to provide water allocation rights. This protocol provides a true sense of water security and financial opportunity by allowing people to redeem their rights. This system not only secures future water allocations, but also increases token scarcity and value.

Additionally, a pure sense of investment is achieved through investments in water sources. This leads to potential financial returns and dividends by addressing the inefficiencies in water supply mentioned above. By investing to finance infrastructure projects, such as building factories and improving distribution systems, more water can be brought to communities, creating additional economic opportunities.

Monetizing water access through the C2B model, the “Burn to Secure” protocol, and investments in water sources all generate economic benefits for the community, promoting a more equitable and efficient water management system.

Overcoming challenges

While blockchain technology has the potential to improve water management, there are challenges to its adoption. The complexity of blockchain systems and the need for technological infrastructure can be barriers, especially in developing regions. Additionally, there are concerns about the significant energy consumption of blockchain networks. However, technological advances and the development of more energy-efficient blockchain solutions are helping to alleviate these concerns. Additionally, education and capacity building are key to ensuring stakeholders understand how to effectively use blockchain technology. Governments, NGOs, and private sector partners need to work together to provide training and support to communities and water management authorities.

Blockchain technology offers a practical and effective means to improve water management. In addition to addressing inefficiencies, blockchain empowers communities, promotes sustainable practices, and opens up new economic opportunities through models like community-to-business (C2B). As we face the growing challenges of climate change and population growth, blockchain is not only an innovative solution, but represents a fundamental shift in the way we manage and value water resources. Adopting blockchain in water management is essential to creating a sustainable and equitable future by changing the way we interact with and protect our most vital resource.

Jean-Hugues Gavarini

Jean-Hugues Gavarini is the CEO and co-founder of LAKE (LAK3), a real-world asset company leveraging blockchain technology to decentralize access to the global water economy. LAKE aims to ensure access to clean water for all, protect water resources, and deliver water to those in need through innovative technologies. Jean-Hugues has a diverse career spanning the luxury, fashion, and footwear industries. His career path includes notable successes at Mellow Yellow, Cremieux, and Tod’s. Raised between Silicon Valley and the French Alps, Jean-Hugues has always been immersed in technology and freshwater resources. In 2018, Jean became the CEO of Lanikea Waters, a water solutions entity based in the French Alps. In 2019, the concept of LAKE was born, embodying his commitment to innovation and sustainability.

With rapid advances in the world of AI and blockchain, there are opportunities to leverage the security and transparency features of blockchain to improve the reliability and trust of AI systems and data transactions.

Explore the synergy of these advanced technologies in virtual mode Blockchain and AI Expowhich takes place on October 31, 2024 TO 10:00 GMT.

The event features cutting-edge presentations led by leading experts in evolving fields. Presentations are set to explore opportunities and challenges in the fusion of blockchain and AI, real-world applications, ethics, innovations in environmental sustainability, and more!

Gain a comprehensive understanding of how these technologies can synergistically drive innovation, optimize operations, and promote strategic growth opportunities. Develop your knowledge to facilitate informed decision making and give your company a competitive edge in the growing technology landscape.

Nigeria is keeping an eye on a new native blockchain network to protect the country’s data sovereignty.

According to local media, a team from the University of Hertfordshire has proposed the new blockchain, Nigeriato the National Information Technology Development Agency (NITDA).

Chanu Kuppuswamy, who leads the team, argued that relying on blockchain networks whose developers are located in other regions poses national security risks to the Nigerian government. He further said that Nigerium would allow the West African nation to customize the network to meet specific needs, while also promoting data sovereignty.

In his presentation, Chanu cited the recent migration of Ethereum to test of participation (PoS) consensus as an instance in which no Nigerians were involved but whose impact is far-reaching.

“Developing an indigenous blockchain like Nigerium is a significant step towards achieving data sovereignty and promoting trust in digital transactions in Nigeria,” he said.

While receiving the proposals in Abuja, NITDA’s Kashifu Abdullahi acknowledged the benefits a local blockchain would bring to Nigeria, including increased security of citizens’ data.

However, a NITDA spokesperson later clarified that Nigerium is still at the proposal stage and that the government has not yet decided whether to proceed or not.

“The committee is still discussing the possibility with stakeholders. Even if a decision is finally made, there is no guarantee that the name will be Nigerium,” the spokesperson told the media.

Nigerium’s reception in the country has been mixed. Some, like financial analyst Olumide Adesina, To say the network is “dead on arrival”. He believes the Nigerian government’s poor record in following through on its big technology plans will claim another victim. He pointed to the eNaira as a missed opportunity whose chances of success were much higher than those of Nigerium.

Others welcomed the proposal. Chimezie Chuta, who chairs the renewed The Nigerian Blockchain Policy Committee is “extremely optimistic“that Nigerium will be more successful than eNaira.

Speaking to a local news agency, Chuta stressed that eNaira failed because the central bank initiated the project on its own, without involving any stakeholders.

“They just cooked it and expected everyone to like it. [With Nigerium]there will be a lot of collaboration,” he said.

Registration of property title, digital identity and Certificate Verification are among the use cases that Nigerium is expected to initially target. However, Nigeria has already made progress in some of these fields through public blockchains.

SPPG, a leading school in governance and politics, announced in May the country’s first blockchain certificate verification system. Built on the The BSV BlockchainIt was developed in collaboration with the blockchain data recording company VX Technologies and local lender Sterling Bank.

Watch: The Future Has Already Arrived in Nigeria

Italian: https://www.youtube.com/watch?v=M40GXUUauLU width=”560″ height=”315″ frameborder=”0″ allowfullscreen=”allowfullscreen”>

Italian: https://www.youtube.com/watch?v=M40GXUUauLU width=”560″ height=”315″ frameborder=”0″ allowfullscreen=”allowfullscreen”>

New to blockchain? Check out CoinGeek Blockchain for Beginners section, the definitive guide to learn more about blockchain technology.

A Japanese fintech developer will build a blockchain-based bond market gateway for Palau, aiming to launch a trial in 2024 and a full launch the following year.

Japanese fintech developer Suramitsubest known for developing a central bank digital currency (CBDC) for Cambodia, is intended to build a Blockchain-gateway to the bond market based on the Pacific island nation of Palau, Nikkei He learned.

Soramitsu won the contract and plans to introduce the market on a trial basis in fiscal 2024, with a full launch scheduled for the following year, allowing the Palauan government to issue bonds to individual investors and efficiently manage principal and interest payments, according to the report.

The total cost of the project is estimated at several hundred million yen ($1.2 million to $5.6 million), less than half the cost of a non-blockchain alternative, people familiar with the matter said. The project has reportedly received support from Japan’s Ministry of Economy, Trade and Industry, with Japan’s foreign and finance ministries providing strategic and management advice on the project.

Soramitsu’s successful development of Cambodia’s CBDC in 2020 has boosted its reputation, with the digital currency’s popularity soaring, with over 10 million accounts opened by December 2023, representing 60% of Cambodia’s population. Following this, Cambodia’s central bank governor Chea Serey indicated intends to expand the reach of its CBDC internationally, particularly through collaboration with UnionPay International, the Chinese card payment service, and other global partners.

While Soramitsu’s work in Cambodia has been well received, the long-term popularity of CBDCs remains to be seen. As of late June, crypto.news reported a sharp drop in activity in India’s digital currency, the e-rupee, after local banks stopped artificially inflating its values.

According to people familiar with the matter, the Reserve Bank of India managed to hit the 1 million retail transaction milestone last December only after the metrics were artificially infiltrated by local banks, which offered incentives to retail users and paid a portion of the bank’s employees’ salaries using the digital currency.

Blockchain Technology Will Transform Water Access and Management Globally

Ethereum Price Hits $3,300, Eyes on $4,000 This Week?

Bitcoin Will Surge to $100K After Q4, Here’s Why

South Korea Moves to Delay Cryptocurrency Tax Until 2028 Amid Market Concerns

Blockchain and AI Expo 2024

“Captain Tsubasa – RIVALS” launches on Oasys Blockchain

Comment deux frères auraient dérobé 25 millions de dollars lors d’un braquage d’Ethereum de 12 secondes • The Register

Solana ranks the fastest blockchain in the world, surpassing Ethereum, Polygon ⋆ ZyCrypto

Historic steps for US cryptocurrencies! With a shocking majority vote!🚨

Is Emorya the next gem💎 of this Bitcoin bull run?

Who shot Donald Trump? BlackRock? Biden? Bitcoin EXPLODES!

5 Altcoins to Buy NOW During This Crypto Crash [100x Potential]

The Next Big Crypto: Beldex (Best Browser & VPN for Privacy)

Cryptocurrency Market About to Turn Upside Down?! (Inflation Data Today, Germany Sells Bitcoin, Solana News)

Crypto Victory in Congress! Ethereum ETF (Trump vs Biden) BIG NEWS

-

News1 year ago

News1 year ago“Captain Tsubasa – RIVALS” launches on Oasys Blockchain

-

Ethereum1 year ago

Ethereum1 year agoComment deux frères auraient dérobé 25 millions de dollars lors d’un braquage d’Ethereum de 12 secondes • The Register

-

News1 year ago

News1 year agoSolana ranks the fastest blockchain in the world, surpassing Ethereum, Polygon ⋆ ZyCrypto

-

Videos1 year ago

Videos1 year agoHistoric steps for US cryptocurrencies! With a shocking majority vote!🚨

-

Videos1 year ago

Videos1 year agoIs Emorya the next gem💎 of this Bitcoin bull run?

-

News1 year ago

News1 year agoSolana Surpasses Ethereum and Polygon as the Fastest Blockchain ⋆ ZyCrypto

-

Videos1 year ago

Videos1 year agoNexus Chain – Ethereum L2 with the GREATEST Potential?

-

Ethereum1 year ago

Ethereum1 year agoScaling Ethereum with L2s damaged its Tokenomics. Is it possible to repair it?

-

News1 year ago

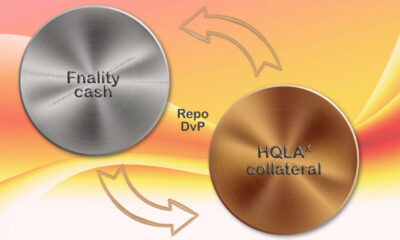

News1 year agoFnality, HQLAᵡ aims to launch blockchain intraday repositories this year – Ledger Insights

-

Regulation1 year ago

Regulation1 year agoFinancial Intelligence Unit imposes ₹18.82 crore fine on cryptocurrency exchange Binance for violating anti-money laundering norms

-

Bitcoin1 year ago

Bitcoin1 year agoBitcoin Drops to $60K, Threatening to Derail Prices of Ether, Solana, XRP, Dogecoin, and Shiba Inu ⋆ ZyCrypto

-

Videos1 year ago

Videos1 year agoRaoul Pal’s Crypto Predictions AFTER Bitcoin Halving in 2024 (The NEXT Solana)